- 2024-10-31T00:00:00

- Company Research

- We anticipate insignificant changes to our 2024F NPAT-MI forecast (VND29.7tn/USD1.2bn; -11% YoY), but we foresee upside potential to our 2024F presales forecast (VND90.7tn/USD3.6bn; +4% YoY), mainly due to stronger-than-expected 9M 2024 presales at the Royal Island project.

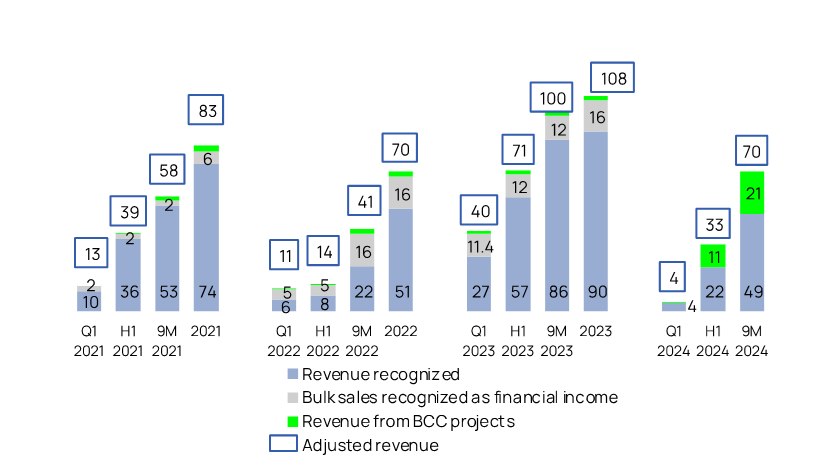

- VHM recorded Q3 2024 results with underlying property revenue (including business cooperation contracts (BCC) and bulk sales transactions recognized as financial income) of VND36tn (USD1.4bn; -7% QoQ and +24% YoY) and NPAT-MI of VND7.9tn (USD315mn; -28% QoQ and -26% YoY), mainly supported by ongoing deliveries at Ocean Park 2 & 3, and the start of handovers to retail buyers at Royal Island recognized in financial income. We attribute the difference in growth between the top-line and bottom-line mainly to a lower gross margin, primarily because the majority of delivered units at Ocean Park 2 & 3 are under BCCs (where VHM shares profits with BCC partners) with lower margins compared to retail/bulk sales, in line with our expectations.

- In 9M 2024, VHM’s underlying property revenue amounted to VND69.8tn (USD2.8bn; -30% YoY) and NPAT-MI was VND19.6tn (USD786mn; -39% YoY), mainly driven by the Royal Island’s bulk sales recognition in Q2 2024 and retail handovers starting from Q3 2024, as well as ongoing handovers at Ocean Park 2 & 3. VHM’s 9M 2024 underlying property revenue and NPAT-MI fulfilled 58% and 66% of our full-year forecasts, respectively.

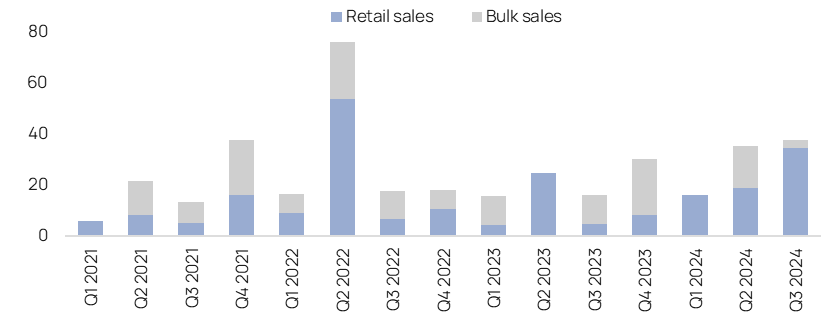

- QoQ growth in Q3 2024 contracted sales driven by strong retail presales: VHM’s Q3 2024 contracted sales value was VND37.9tn (USD1.5bn; +7% QoQ and +135% YoY), with retail presales accounting for 91%. Key contributors for Q3 2024 presales included retail presales at Royal Island, Golden Avenue, and Ocean Park 3, and one bulk sales transaction in Ocean Park 3. VHM’s 9M 2024 contracted sales value was VND89.6tn (USD3.6bn; +58% YoY), with the Royal Island contributing 67%.

- In March 2024, VHM launched the Royal Island project in Hai Phong Province (with a total size of 877 ha and 8,300 low-rise units & 1,700 commercial shophouses). At end-Q3 2024, around 3,800 units at this project have been presold to retail buyers (equivalent to 90% of launched units). The company started to hand over presold units at this project in September, with ~1,300 units delivered for retail buyers in the quarter.

- In September 2024, VHM held an introduction event for the Global Gate project in Hanoi (with a total size of 385 ha, 4,100 low-rise and 12,600 high-rise units). The official presales for this project have not yet been provided and are not included in VHM’s Q3 2024 contracted sales.

- As of end-Q3 2024, VHM’s unbilled bookings amounted to VND123tn (USD4.9bn; +60% YoY) with bulk sales accounting for 53%. Management expects the main drivers for Q4 2024G earnings to be ongoing deliveries at Ocean Park 3 and Royal Island, as well as the recognition of potential bulk sales transactions.

- New corporate bond issue plans: On October 29 and 30, 2024, VHM announced plans to issue new domestic and international corporate bonds as follows:

- Domestic bond: Up to VND4tn (USD160mn); maximum 3 years; secured bonds; fixed rate. In 9M 2024, VHM issued VND14.3tn (USD572mn) in domestic bonds.

- International bond: Up to USD500mn; maximum 5 years; non-convertible, non-warrant linked, and unsecured bonds; interest rate not disclosed yet. Previously, at VHM’s 2023 AGM, shareholders approved a plan to issue up to USD500mn in bonds on the Singapore Stock Exchange with a maximum 5-year maturity and no disclosed coupon rate, but the issuance, initially expected by April 2024, had not yet been executed.

- VHM’s net D/E was 22.1% at end-Q3 2024 vs 24.0% at end-Q2 2024 and 21.2% at end-2023. As of end-Q3 2024, VHM’s total debt balance was VND72.2tn (USD2.9bn; +2.4% QoQ and +27.3% YTD), with USD-denominated debts accounting for 11% of the total debt. The current portion of long-term debts maturing within 12 months included (1) bank loans of VND4.4tn (USD176mn) and (2) corporate bonds of VND3.8tn (USD151mn). As of end-Q3 2024, VHM has no international bond balance.

Figure 1: VHM’s 9M 2024 results

VND bn | 9M 2023 | 9M 2024 | YoY | 2024F | 9M 2024 as | Vietcap’s comments on 9M 2024 results |

Net revenue | 94,636 | 69,910 | -26% | 108,384 | 65% |

|

| 85,737 | 48,777 | -43% | 91,442 | 53% | * VHM’s 9M 2024 underlying property revenue (including BCC and bulk sales transactions recognized as financial income) amounted to VND69.8tn (USD2.8bn; -30% YoY), with Royal Island contributing 29%, Ocean Park 3 at 26%, and Ocean Park 2 at 18%. |

| 8,899 | 21,133 | 137% | 16,942 | 125% | * Mainly construction and leasing services. |

|

|

|

|

|

|

|

Gross profit | 34,708 | 20,214 | -42% | 34,850 | 58% |

|

| 33,286 | 17,964 | -46% | 32,688 | 55% |

|

| 1,421 | 2,250 | 58% | 2,162 | 104% |

|

|

|

|

|

|

|

|

SG&A expenses | -4,758 | -5,400 | 13% | -5,425 | 100% |

|

EBIT | 29,950 | 14,814 | -51% | 29,425 | 50% |

|

Financial income | 15,560 | 15,536 | 0% | 14,924 | 104% |

|

| 989 | 10,651 | 977% | 9,249 | 115% | * Includes Royal Island’s bulk sales recognition in Q2 2024 with a pre-tax gain of VND6.4tn (USD251mn) and retail handovers starting from Q3 2024 with ~1,300 units delivered in the quarter. |

| 14,571 | 4,885 | -66% | 5,675 | 86% |

|

Financial expense | -2,238 | -5,477 | 145% | -6,464 | 85% |

|

Other gain/loss | -1,351 | -279 | N.M. | -200 | N.M. |

|

PBT | 41,920 | 24,596 | -41% | 37,685 | 65% |

|

PAT | 32,396 | 20,600 | -36% | 30,148 | 68% |

|

NPAT-MI | 32,300 | 19,642 | -39% | 29,726 | 66% | * 9M 2024 NPAT-MI was supported by the Royal Island’s bulk sales recognition in Q2 2024 and retail handovers starting from Q3 2024, as well as ongoing deliveries at Ocean Park 2 & 3. |

|

|

|

|

|

|

|

Gross margin % | 36.7% | 28.9% |

| 32.2% |

|

|

| 38.8% | 36.8% |

| 35.7% |

|

|

| 16.0% | 10.6% |

| 12.8% |

|

|

SG&A as % sales | 5.0% | 7.7% |

| 5.0% |

|

|

EBIT margin % | 31.6% | 21.2% |

| 27.1% |

|

|

Effective tax rate % | 22.7% | 16.2% |

| 20.0% |

|

|

NPAT-MI margin % | 34.1% | 28.1% |

| 27.4% |

|

|

Source: VHM, Vietcap forecast (last updated August 15, 2024). Note: (*) Vingroup signed a business cooperation contract (BCC) with VHM to fully transfer the economic interest of real estate developments that are not injected into VHM due to the complexity of paperwork. Thus, VHM records all gains via financial income.

Figure 2: Property segment’s revenue (VND tn)

Unbilled bookings as of end-Q3 2024: VND123tn (USD4.9bn)

Source: VHM, Vietcap compilation. Note: Adjusted revenue includes (1) revenue recognized as property revenue, (2) revenue from BCC, and (3) bulk sales recognized as financial income.

Figure 3: Quarterly contracted sales results (VND tn)

Source: VHM, Vietcap compilation

Powered by Froala Editor