- 2024-07-18T00:00:00

- Company Research

- VHM recorded Q2 2024 NPAT-MI of VND10.8tn (USD423mn; +12x QoQ and +11% YoY), mainly supported by i) the recognition of bulk sales at the Royal Island project with a total pre-tax gain of VND6.4tn/USD251mn and ii) handovers at Ocean Park 1, 2, 3, and Golden Avenue.

- In H1 2024, VHM’s underlying property revenue (including business cooperation contract (BCC) and bulk sales transactions recognized as financial income) amounted to VND33.4tn (USD1.3bn; -52% YoY) and NPAT-MI was VND11.7tn (USD458mn; -46% YoY), mainly driven by the bulk sales recognition in Q2 2024, completing 29% and 40% of our 2024F respective forecasts.

- We foresee insignificant changes to our 2024F NPAT-MI of VND29.4tn (USD1.2bn; -12% YoY), as the higher-than-expected gross profit of other services and interest income can offset the higher-than-expected financial expenses in H1 2024, pending a fuller review.

- Strong Q2 2024 contracted sales were driven by both sustained QoQ improvement in retail presales and new bulk sales at the Royal Island. VHM’s Q2 2024 contracted sales value was VND35.5tn (USD1.4bn; +120% QoQ and +43% YoY), with retail presales (accounting for 53%) increasing 17% QoQ in Q2 2024 and driven by the recently-launched Royal Island project. In March, VHM launched the Royal Island project in Hai Phong Province (with a total size of 877 ha & 8,300 low-rise units). At end-Q2 2024, around 2,800 units at this project have been presold to retail buyers, equivalent to 90% of total launched units.

- H1 2024’s contracted sales value was VND51.7tn (USD2.0bn; +27% YoY), with the Royal Island contributing 81%. Per management, as of June 2024, VHM is in the process of finalizing two potential bulk sales transactions with a total deal size of around VND40tn (USD1.6bn). We foresee potential upside to our 2024F contracted sales value of VND77.4tn (USD3.0bn; -11% YoY) due to H1 2024 better-than-expected presales at the Royal Island.

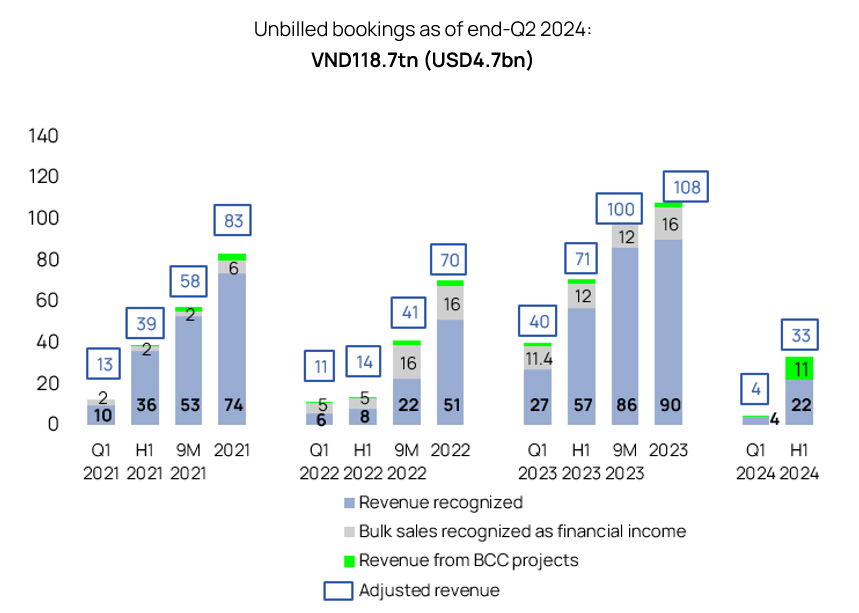

- As of end-Q2 2024, VHM’s unbilled bookings amounted to VND118.7tn (USD4.7bn; +33% YoY) with bulk sales accounting for 58%. Management expects 55% of the unbilled bookings to be recognized in H2 2024G.

- Management plans to launch two new projects in Hanoi in H2 2024G – Co Loa (385 ha, mainly high-rise units) and Wonder Park (133 ha, mainly low-rise units), along with the continued presales at its launched projects. In addition, in July 2024, VHM launched The Royal Residence (the high-rise component in Vinhomes Star City Thanh Hoa) and recorded its first launch's take-up rate of 70% within five days.

- Vinhomes Vung Ang Industrial Park (IP) received investment approval. VHM currently has one operating IP, VinFast Manufacturing Complex in Hai Phong (total site area of 276 ha; occupancy rate of 100%) and several IPs/industrial clusters in the pipeline - mainly in the provinces of Hai Phong, Quang Ninh, and Ha Tinh. On July 13, the Deputy Prime Minister signed a decision for the investment approval of the Vinhomes Vung Ang IP (965 ha of total site area; Ha Tinh). We currently do not factor in the operational/potential IP development segment into our earnings forecast as we expect there to be minor contributions from IPs into VHM’s 2024-2026F profit outlook.

Figure 1: VHM’s H1 2024 results

VND bn | H1 2023 | H1 2024 | YoY | 2024F | H1 2024 as | Vietcap’s comments on H1 2024 results |

Net revenue | 61,912 | 36,429 | -41% | 123,244 | 30% |

|

| 56,825 | 21,927 | -61% | 112,301 | 20% | * VHM’s H1 2024 underlying property revenue (including BCC and bulk sales transactions recognized as financial income) amounted to VND33.4tn (USD1.3bn; -52% YoY), completing 29% of our 2024F forecast. * Key deliveries in H1 2024 included the Ocean Park 1, 2, 3, and Golden Avenue projects. * We attribute the difference in VHM’s reported net revenue/gross margin for property segment and VHM’s financial income vs our forecasts mainly to our assumption that all bulk sales transactions in 2024F will be recorded into net revenue and EBIT. |

| 5,088 | 14,502 | 185% | 10,942 | 133% | * Mainly construction services. |

|

|

|

|

|

| |

Gross profit | 19,751 | 10,089 | -49% | 45,854 | 22% |

|

| 18,772 | 8,604 | -54% | 43,993 | 20% |

|

| 979 | 1,485 | 52% | 1,862 | 80% |

|

|

|

|

|

|

|

|

SG&A expenses | -3,439 | -2,557 | -26% | -7,094 | 36% |

|

EBIT | 16,312 | 7,532 | -54% | 38,760 | 19% |

|

Financial income | 13,715 | 10,080 | -27% | 3,759 | 268% |

|

| 968 | 6,541 | 576% | 462 | 1415% | * Mainly the bulk sales recognition at the Royal Island project (under BCC with VIC; where VHM holds a 95% economic interest) with total pre-tax gain of VND6.4tn (USD251mn) in Q2 2024. |

| 12,747 | 3,539 | -72% | 3,297 | 107% |

|

Financial expense | -1,284 | -3,827 | 198% | -5,648 | 68% |

|

Other gain/loss | -1,029 | -123 | N.M. | 0 | N.M. |

|

PBT | 27,714 | 13,664 | -51% | 36,871 | 37% |

|

PAT | 21,672 | 11,513 | -47% | 29,497 | 39% |

|

NPAT-MI | 21,605 | 11,669 | -46% | 29,362 | 40% | * H1 2024 NPAT-MI was supported by the bulk sales recognition at the Royal Island project in Q2 2024 and property handovers from the unbilled bookings. |

|

|

|

|

|

| |

Gross margin % | 31.9% | 27.7% |

| 37.2% |

|

|

| 33.0% | 39.2% |

| 39.2% |

|

|

| 19.2% | 10.2% |

| 17.0% |

|

|

SG&A as % sales | 5.6% | 7.0% |

| 5.8% |

|

|

EBIT margin % | 26.3% | 20.7% |

| 31.5% |

|

|

Effective tax rate % | 21.8% | 15.7% |

| 20.0% |

|

|

NPAT-MI margin % | 34.9% | 32.0% |

| 23.8% |

|

|

Source: VHM, Vietcap forecast (last updated May 17, 2024). Note: (*) Vingroup signed a business cooperation contract (BCC) with VHM to fully transfer the economic interest of real estate developments that are not injected into VHM due to the complexity of paperwork. Thus, VHM records all gains via financial income.

Figure 2: Property segment’s revenue (VND tn)

Source: VHM, Vietcap compilation. Note: Adjusted revenue includes (1) revenue recognized as property revenue, (2) revenue from BCC, and (3) bulk sales recognized as financial income.

Powered by Froala Editor