- 2024-07-31T00:00:00

- Company Research

- Q2 NPAT-MI came in at VND1.2tn (+48% YoY, + 12% QoQ) with revenue of VND73.8tn (+12% YoY; -2% QoQ). This is mainly driven by sales volume increasing 1% YoY (from Q2 2023 high base), GPM expansion from 5.9% to 6.3%, and one-off profit of VND121bn. The Q2 Brent oil price experienced a downward trend for most of Q2 vs a general upward trend in Q1, however, the average price was USD85/bbl (+9% YoY, 4% QoQ) vs Q1’s average of USD82/bbl. We attribute the robust profit to PLX’s strong capability in sourcing inputs, insignificant forex loss, and insignificant inventory provisions/write-backs.

- H1 revenue and NPAT-MI were VND148.9tn (+12% YoY) and VND2.3tn (+59% YoY), completing 52% and 60% of our respective full-year forecasts.

- We expect significantly higher H2 NPAT vs H1 with the MoIT (Ministry of Industry & Trade) & MoF’s (Ministry of Finance) recent upward adjustment in regulated costs, equaling 6% (2x the increase in 2023) for gasoline and 14% (4.7x the increase in 2023) for diesel, effective from July 4, in addition to 2% higher estimated sales volume than in H1.

- Additionally, the MoIT will submit the revised Decree on the petroleum industry to the Government for approval within Q3. We currently expect the new Decree to help petroleum distributors to better cover their operating costs and strengthen their profitability further. Previously, the MoIT released a new, third draft of the decree to revise Decree 83/2014, Decree 95/2021, and Decree 80/2023. Overall, the third draft maintains the aims of the second draft in terms of: (1) allowing petrol distributors to set their own prices within a ceiling set by the Government, and (2) reducing intermediaries.

- We see upside potential to our 2024 NPAT forecast, pending a fuller review. We currently have a BUY rating for PLX with a target price of VND55,000/share.

Figure 1: PLX’s H1 2024 results

VND bn | Q2 2023 | Q2 2024 | YoY | H1 2023 | H1 2024 | YoY | % of Vietcap’s 2024F |

Brent oil price (USD/bbl) * | 78 | 85 | 9% | 80 | 83 | 4% | 100% |

Gasoline price (VND/liter) * | 21,385 | 22,711 | 6% | 21,736 | 22,490 | 3% | 116% |

Diesel price (VND/liter) * | 18,540 | 20,362 | 10% | 19,858 | 20,437 | 3% | 106% |

Domestic sales volume (mn m3) | 2.66 | 2.67 | 0.5% | 5.27 | 5.30 | 0.5% | 49% |

Revenue | 65,750 | 73,837 | 12% | 133,182 | 148,943 | 12% | 52% |

Gross profit | 3,931 | 4,621 | 18% | 7,490 | 9,291 | 24% | 51% |

Selling expense | -2,958 | -3,209 | 8% | -5,766 | -6,407 | 11% | 51% |

G&A expense | -219 | -253 | 15% | -426 | -491 | 15% | 48% |

Operating profit | 753 | 1,159 | 54% | 1,298 | 2,392 | 84% | 54% |

Financial income | 432 | 430 | 0% | 946 | 880 | -7% | 48% |

Financial expenses | -355 | -373 | 5% | -737 | -748 | 1% | 52% |

Interest expenses | -230 | -177 | -23% | -463 | -371 | -20% | 35% |

Profit/(loss) from JVs, associates | 193 | 166 | -14% | 343 | 277 | -19% | 44% |

PBT | 1,064 | 1,503 | 41% | 1,902 | 2,944 | 55% | 56% |

Income tax | -172 | -228 | 33% | -344 | -537 | 56% | 51% |

Reported NPAT-MI | 813 | 1,199 | 48% | 1,433 | 2,272 | 59% | 60% |

|

|

| Δ ppts |

|

| Δ ppts |

|

Gross profit margin % | 6.0% | 6.3% | +0.3 | 5.6% | 6.2% | +0.6 |

|

Sales & marketing % sales | 4.5% | 4.3% | -0.2 | 4.3% | 4.3% | -0.0 |

|

General admin % sales | 0.3% | 0.3% | +0.0 | 0.3% | 0.3% | +0.0 |

|

EBIT Margin | 1.1% | 1.6% | +0.4 | 1.0% | 1.6% | +0.6 |

|

NPAT-MI margin | 1.2% | 1.6% | +0.4 | 1.1% | 1.5% | +0.4 |

|

Source: PLX, Vietcap (*average prices)

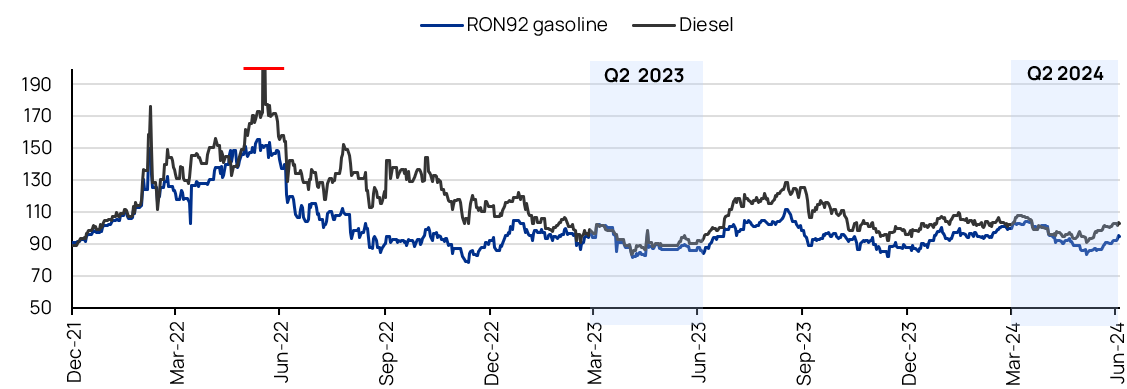

Figure 2: Platts Singapore price movement (reference point for Vietnamese petroleum retail prices), excluding the impact of the petroleum stabilization fund (USD/bbl)

Source: Ministry of Industry and Trade, Vietcap (data as of June 30, 2024)

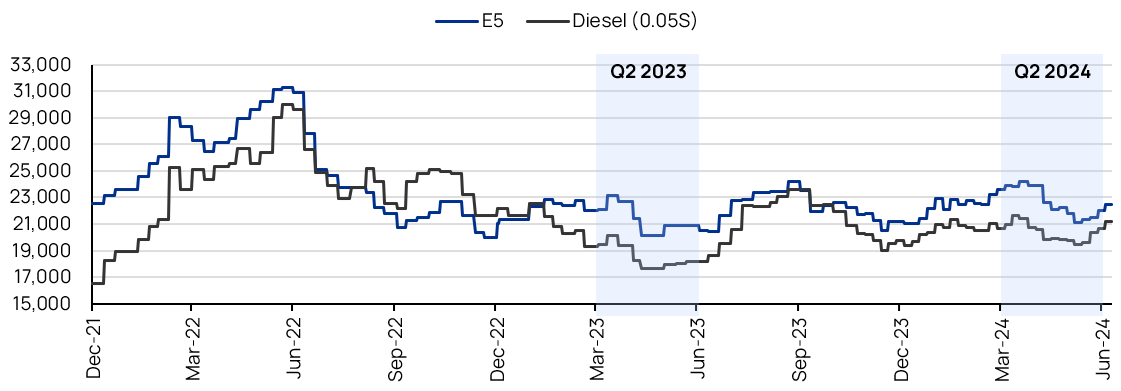

Figure 3: Vietnamese E5 gasoline and diesel retail prices, including the impact of the petroleum stabilization fund (VND/liter)

Source: PLX, Vietcap (data as of June 30, 2024)

Powered by Froala Editor